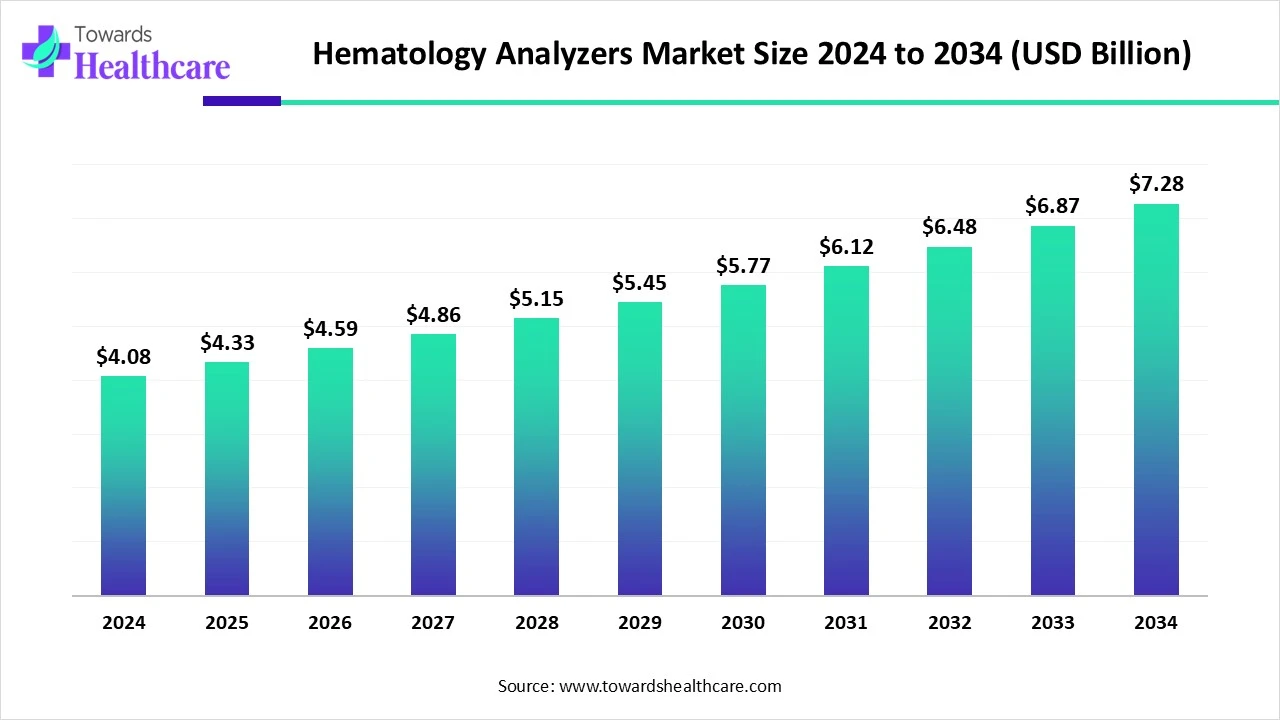

Hematology Analyzers Market Size to Attain USD 7.28 Bn by 2034, Driven by Rising Blood Disorders and Adoption of Automated Diagnostics

The global hematology analyzers market size is calculated at USD 4.33 billion in 2025 and is expected to reach around USD 7.28 billion by 2034, growing at a CAGR of 5.97% for the forecasted period.

Ottawa, Oct. 27, 2025 (GLOBE NEWSWIRE) — The global hematology analyzers market size was valued at USD 4.08 billion in 2024 and is predicted to hit around USD 7.28 billion by 2034, rising at a 5.97% CAGR, a study published by Towards Healthcare a sister firm of Precedence Research.

This market is rising because of a surge in blood-related disorders, growing preventive healthcare awareness, and rapid integration of advanced automated diagnostics across healthcare settings.

The Complete Study is Now Available for Immediate Access | Download the Sample Pages of this Report @ https://www.towardshealthcare.com/download-sample/5838

Key Takeaways:

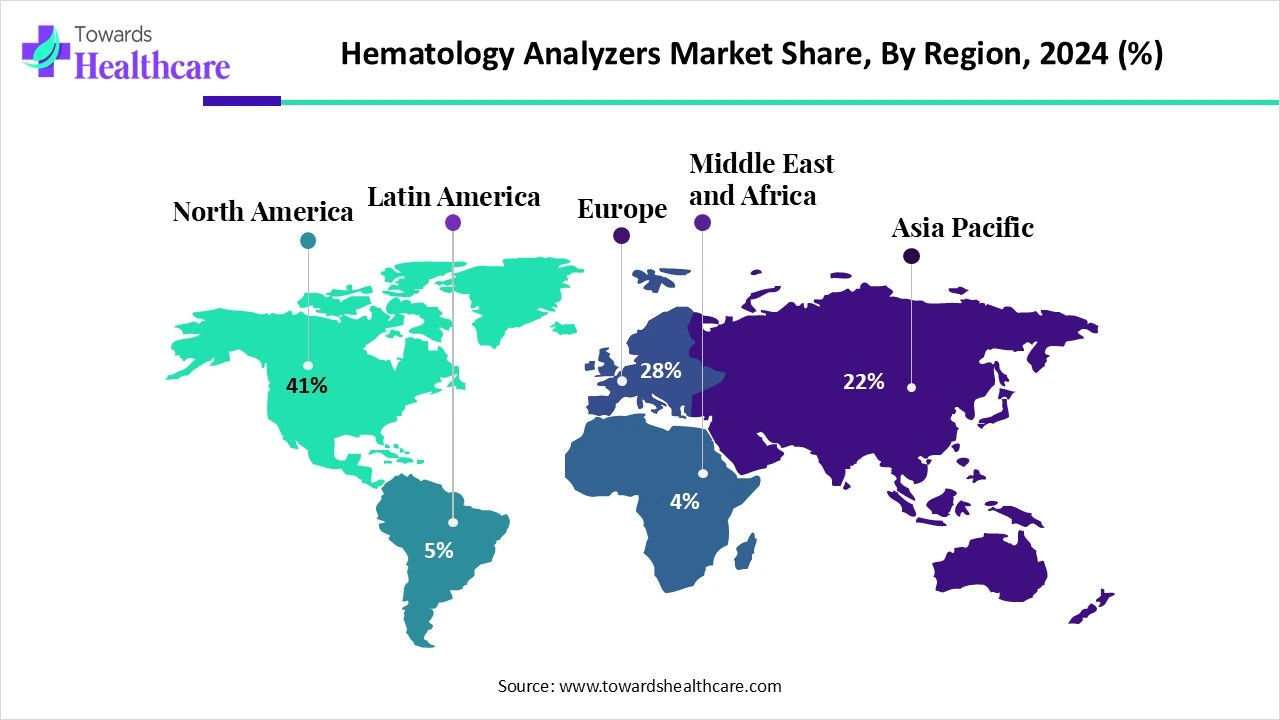

- North America led the market with approximately 41% revenue share in 2024.

- Asia Pacific is expected to grow at the fastest CAGR in the upcoming years.

- By product type, the 5-part differential hematology analyzers segment held a ~51% share of the global hematology analyzers market in 2024.

- By product type, the 6-part and above/high-end analyzers segment is expected to be the fastest-growing during 2025-2034.

- Shape, PictureBy technology, the flow cytometry-based analyzers segment was dominant (~46%) in the market in 2024.

- Shape, PictureBy technology, the artificial intelligence & machine learning integration segment is expected to expand rapidly over the forecast period.

- By application, the complete blood count (CBC) segment held the largest revenue share of nearly 58% in 2024.

- By application, the coagulation & platelet studies segment is expected to register the fastest growth in the predicted timeframes.

- By end user, the hospitals segment dominated with a ~42% share of the global hematology analyzers market in 2024.

- By end user, the ambulatory surgical centers & physician offices segment is expected to be the fastest-growing during the 2025-2034 period.

- Shape, PictureBy modality, the standalone hematology analyzers segment led the market in 2024.

- Shape, PictureBy modality, the integrated systems with immunoassay/chemistry platforms segment is expected to grow at a rapid CAGR in the upcoming years.

Market Overview:

Hematology analyzers contain automated devices used to obtain complete blood counts (CBC), differential leukocyte counts, platelet and coagulation studies, and other tests related to hematology. The market drivers include the increasing incidence of hematological disorders, advances in technology (automation, AI, flow cytometry), and worldwide expansion of diagnostics infrastructure.

The market demands are shaped by increasing utilization in hospitals, laboratories and point-of-care settings, as healthcare systems prioritize early evaluation and enable high throughput screening. In summary, the market is progressing from simple cell counters to multi-parameter analyzers and integrated diagnostic platforms, to reflect clinical complexity and increasing need for automation.

You can place an order or ask any questions, please feel free to contact us at [email protected]

Key Metrics and Overview

| Metric | Details | |

| Market Size in 2025 | USD 4.33 Billion | |

| Projected Market Size in 2034 | USD 7.28 Billion | |

| CAGR (2025 – 2034) | 5.97 | % |

| Leading Region | North America Share by 41% | |

| Market Segmentation | By Product Type, By Technology, By Application, By End User, By Modality, By Region | |

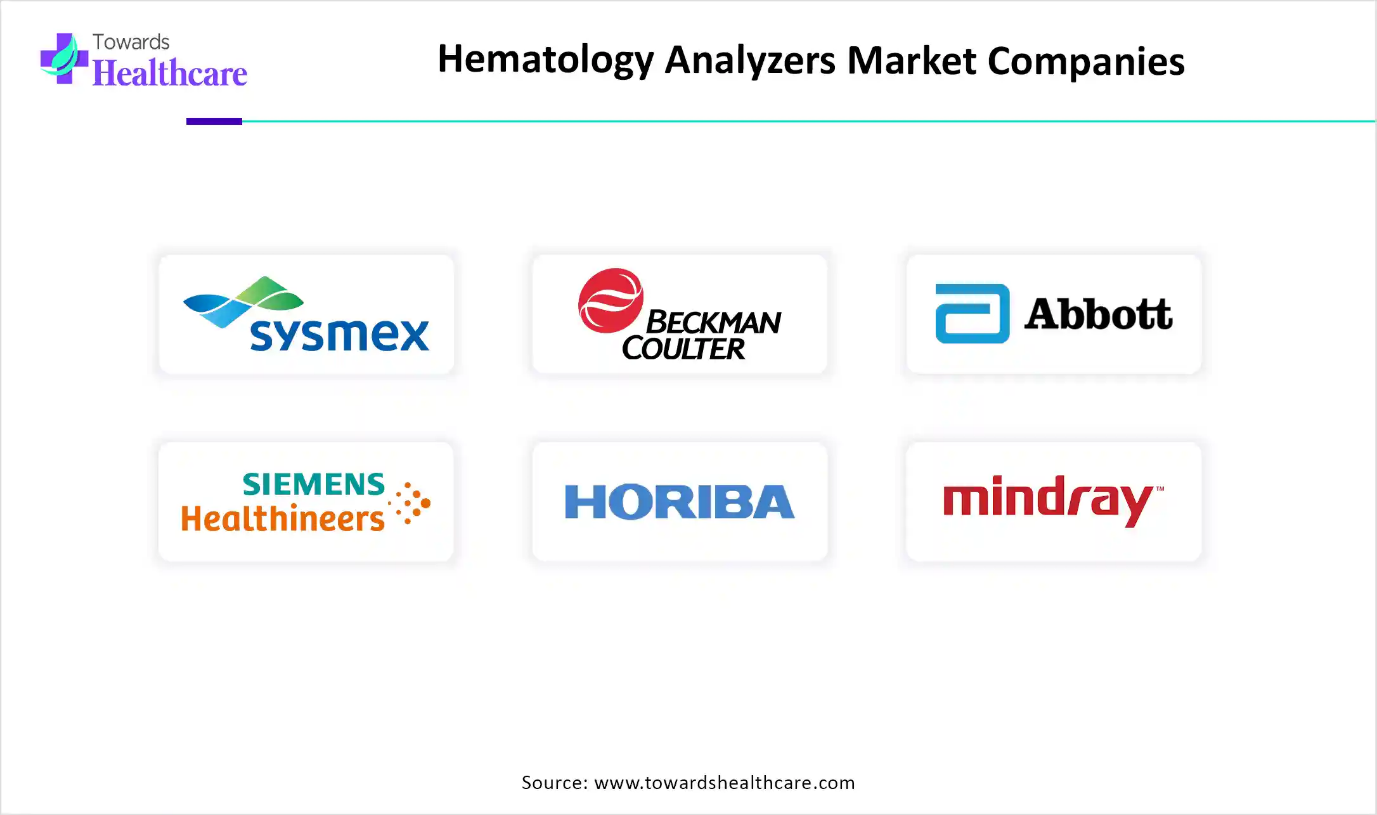

| Top Key Players | Sysmex Corporation, Beckman Coulter, Abbott Laboratories, Siemens Healthineers, Horiba Ltd., Mindray Medical International Limited, Bio-Rad Laboratories, Inc., Roche Diagnostics, Boule Diagnostics AB, Diatron MI Zrt., Nihon Kohden Corporation, Ortho Clinical Diagnostics, Drucker Diagnostics, PixCell Medical Technologies, Dymind Biotechnology Co., Ltd., Heska Corporation, Agappe Diagnostics, Dirui Industrial Co., Ltd., Erba Mannheim, Thermo Fisher Scientific | |

Major Growth Drivers:

Which are the important aspects that are promoting the growth of the hematology analyzer market?

- The increasing prevalence of hematologic disorders, including anemia, leukemia, thrombocytopenia and other blood-cell disorders, is increasing the demand for hematology testing globally, particularly with the growing aging population and chronic disease burden.

- Healthcare systems are adopting more preventative diagnostic screening and routine complete blood count (CBC) screening, facilitating the demand for higher throughput and reliability of hematology analyzers across hospitals and laboratories.

- Analyzers are often seen as platforms for technology innovation that increases accuracy, speed and productivity increasing the uptake of new systems.

- The expanding diagnostic infrastructure in emerging geographies coupled with growing health expenditures, lab upgrades and greater accessibility to diagnostics expands growth opportunities.

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

Key Drifts:

What are Major Drifts in Hematology Analyzers Market?

The hematology analyzers market is experiencing a trend towards higher throughput and modular automation, which has 8-part differential analyzers and long automation tracks. Additionally, it is becoming common to see adoption of artificial intelligence and machine-learning algorithms in hematology instrumentation to support blood smear image analysis, establish classification of cell morphology and optimize workflows, all situating hematology in digital-first framework. In developing economies, smaller, and mid-size labs are phasing-out older 3-part differential analyzers in favor of more sophisticated 5- or 6-part analyzers and this is continuing to drive a replacement cycle as well as progress into capital upgrades.

Significant Challenge:

High Equipment and Operational Costs to Create Challenge for the Market

High Equipment and Operating Cost Affecting Emerging Market Adoption The high cost of ownership of advanced equipment and operating costs is a challenge for adoption in low- and middle-income countries and small laboratories. The requirement for trained personnel to operate complex systems and interpret advanced results poses another barrier and moves adoption forward slower in many emerging markets. This impediment of costs and trained personnel could limit growth in poorly resourced markets unless lower-cost easy-to-use devices are developed.

Regional Analysis:

North America Hematology Analyzers Market Trends:

The North American market is expected to have the highest share in the hematology analyzers market by 41% due to a robust healthcare infrastructure, opportunities for high volumes of diagnostics tests and also a large number of hematology analyzers largely manufactured by firms based in North America itself. Furthermore, a supportive structure of regulatory standards and reimbursement regulations are available to help improve the investment into critical advance diagnostic equipment. The high frequency of testing in oncology, chronic blood disorders and health screenings means that labs in this part of the world would be first to invest in high-tech analyzer platforms.

Asia-Pacific Hematology Analyzers Market Trends:

On the other hand, the Asia-Pacific region is poised to be the fastest growing segment of the hematology analyzers market. Expanding healthcare infrastructure including curriculums to train more doctors and nurses, growing middle-income populations, increasing government funding and ability to focus on screening and diagnostics, and upgrading laboratory equipment has become standard practice with many countries such as China, India, and several Southeast Asian nations, investing in laboratory automation, and crowning old “legacy” cell counters for newer analyzer systems. Market reports suggest the Asia-Pacific regional market segment will have higher CAGR as compared to mature market countries. The expansion toward more frequent and routine annual health check-ups have led to higher testing frequencies.

Download the single region market report @ https://www.towardshealthcare.com/checkout/5838

Segmental Insights:

By Product Type:

The 5-part differential hematology analyzers made up roughly 51% of the worldwide hematology analyzers market share. They hold this majority largely because they meet the demands for more detailed leukocyte profiling that is critical to diagnosing infections, inflammatory diseases, hematologic malignancies and monitoring therapy. The 5-part analyzers are a compromise between cost and performance, providing hospitals with a solution that is satisfactory for their work flow, making these analyzers the best option for mid- to high-volume laboratories.

The 6-part and greater (high-end) analyzers is expected to be the fastest growing product type during the time frame of 2025-2034. These analyzers provide even richer data and additionally use more advanced technologies such as flow cytometry and digital morphology. As clinical laboratories in developing markets expand their operations and as clinical care becomes more complex, demand for high-end analyzers will grow.

By Technology:

The segment of analyzers based on flow cytometry was dominant in the market. The benefit of flow cytometry is the ability to evaluate multiple physical and chemical cellular parameters at a single-cell level for more thorough hematologic and immunophenotyping evaluation compared to traditional impedance or optical techniques. Furthermore, flow cytometry maintained a substantial foothold given the strength of the diagnostic capabilities in areas such as hematology, oncology, and high complexity diagnostics. The demand for high sensitivity and specificity, combined with its ability to bring all aspects to the dedicated platforms with machines, and the draw of ease of use reinforce the share of flow cytometry in hematology analyzers.

The segment of the artificial intelligence & machine-learning integration, is projected to grow rapidly over the forecast period. Integrated AI/ML capabilities introduce increasingly sophisticated features for automated cell morphology review, anomaly detection, workflow optimization, and remote digital slide review, coalescing efficiency and reduction in manual labor, running time, and turnaround time, based on testing volume and the type of testing. As laboratories increasingly seek solutions to enhance scale and manage competing for skilled laboratory workforce, exams and instruments that use AI/ML have enhanced appeal as an alternative.

By Application:

The complete blood count (CBC) segment accounted for the largest revenue share, nearly 58%. CBC tests are the foundation of hematology diagnostics as they are some of the most frequently ordered laboratory tests in the world, used in routine health screenings, pre-operative evaluations, chronic disease management, and diagnosis workups. Because CBC tests are a standard part of medical practice and relatively low-cost, CBC tests have a very large demand base and constitute the majority of hematology analyzer use.

The coagulation & platelet studies segment is predicted to have the highest growth rate in the projected time frames. With an increasing awareness of coagulation disorders and platelet-count abnormalities and greater adoption of personalized medicine and anticoagulation testing, laboratories will purchase more analyzers specifically dedicated to platelet function and aggregation, along with coagulation marker tests. In this area, this application segment requires sophisticated instruments and these studies often utilize hematology analyzers.

Get the latest insights on life science industry segmentation with our Annual Membership: https://www.towardshealthcare.com/get-an-annual-membership

By End User:

The hospitals segment held a substantial share of nearly 42% of the global hematology analyzers market by end user in 2024; hospitals are the largest volume users of hematology analyzers as they perform significant numbers of diagnostic tests in multiple contexts, including acute care, inpatient, outpatient, and surgical settings. Hospitals have large laboratories, are likely to upgrade their instrumentation frequently, and often require workflows that are integrated with laboratory systems and high throughput.

The ambulatory surgical centres & physician offices end user is anticipated to be the fastest growing from 2025-2034. These environments are increasingly adopting point-of-care or smaller-footprint hematology analyzers to support rapid turnaround in cost-efficient outpatient care, pre-operative tests, and procedural laboratories. The demand for compact hematology analyzers will continue to improve as providers move care from main hospitals to outpatient settings and physician offices seek to improve operational efficiency and save costs with in-house diagnostics.

By Modality:

The standalone hematology analyzers segment was the market leader in 2024. Standalone analyzers, which are defined as instrumentation dedicated to hematology testing and not integrated models, continue to represent the bulk of installed models and revenue, because many labs prefer to have dedicated hematology testing because they can have higher throughput, easier maintenance, and a lower total cost of ownership than integrated systems.

The integrated systems with immunoassay/chemistry platforms segment is forecasted to grow at a rapid CAGR in the coming years. Integrated platforms (hematology, immunoassay, chemistry and sometimes hemostasis) may provide operational efficiencies, reduce instrument footprint in the lab, enable single-point servicing, and optimize workflow. Labs want to consolidate instrumentation over time and are pursuing instruments that are integrated and reduce complexity and thus the demand for integrated systems will increase market share of analyzer purchasing over time.

Browse More Insights of Towards Healthcare:

The global breath analyzers market size is calculated at US$ 1.022 billion in 2024, grew to US$ 1.2 billion in 2025, and is projected to reach around US$ 5.12 billion by 2034. The market is expanding at a CAGR of 17.44% between 2025 and 2034.

The global veterinary hematology analyzers market size is calculated at US$ 1.01 in 2024, grew to US$ 1.07 billion in 2025, and is projected to reach around US$ 1.72 billion by 2034. The market is expanding at a CAGR of 5.44% between 2025 and 2034.

The global bioprocess analyzers market size is calculated at US$ 2.28 in 2024, grew to US$ 2.54 billion in 2025, and is projected to reach around US$ 6.77 billion by 2034. The market is expanding at a CAGR of 11.54% between 2025 and 2034.

The molecular interaction analyzer market was estimated at US$ 300 million in 2023 and is projected to grow to US$ 575.4 million by 2034, rising at a compound annual growth rate (CAGR) of 6.1% from 2024 to 2034. The growing research & development activities, increasing investments, and latest innovations drive the market.

Recent Developments:

In April 2025, Sysmex Corporation inaugurated its new manufacturing base in India and began full-scale production of its XQ-Series Automated Hematology Analyzer to align with “Make in India” policy and capture emerging market share.

Hematology Analyzers Market lKey Players List:

- Sysmex Corporation

- Beckman Coulter (Danaher Corporation)

- Abbott Laboratories

- Siemens Healthineers

- Horiba Ltd.

- Mindray Medical International Limited

- Bio-Rad Laboratories, Inc.

- Roche Diagnostics

- Boule Diagnostics AB

- Diatron MI Zrt. (Stratec Biomedical)

- Nihon Kohden Corporation

- Ortho Clinical Diagnostics

- Drucker Diagnostics

- PixCell Medical Technologies

- Dymind Biotechnology Co., Ltd.

- Heska Corporation (veterinary segment)

- Agappe Diagnostics

- Dirui Industrial Co., Ltd.

- Erba Mannheim (Transasia Bio-Medicals Ltd.)

- Thermo Fisher Scientific (hematology reagents & kits)

Download the Competitive Landscape market report @ https://www.towardshealthcare.com/checkout/5838

Segments Covered in the Report

By Product Type

- 3-Part Differential Hematology Analyzers

- 5-Part Differential Hematology Analyzers

- 6-Part and Above / High-End Analyzers

- Point-of-Care Hematology Analyzers

- Hematology Reagents & Consumables

By Technology

- Impedance-Based Analyzers

- Flow Cytometry-Based Analyzers

- Digital Imaging Technology

- Artificial Intelligence & Machine Learning Integration

- Microfluidics (for miniaturized & portable analyzers) Shape, Picture

By Application

- Complete Blood Count (CBC)

- Hemoglobin & Hematocrit Analysis

- Reticulocyte Count

- White Cell Differential Count

- Coagulation & Platelet Studies

By End User

- Hospitals

- Clinical Diagnostic Laboratories

- Research & Academic Institutes

- Blood Banks

- Ambulatory Surgical Centers & Physician Offices

By Modality

- Standalone Hematology Analyzers

- Integrated Systems with Immunoassay/Chemistry Platforms

By Region

- North America

- U.S.

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Thailand

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Sweden

- Denmark

- Norway

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa (MEA)

- South Africa

- UAE

- Saudi Arabia

- Kuwait

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/checkout/5838

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

About Us

Towards Healthcare is a leading global provider of technological solutions, clinical research services, and advanced analytics, with a strong emphasis on life science research. Dedicated to advancing innovation in the life sciences sector, we build strategic partnerships that generate actionable insights and transformative breakthroughs. As a global strategy consulting firm, we empower life science leaders to gain a competitive edge, drive research excellence, and accelerate sustainable growth.

You can place an order or ask any questions, please feel free to contact us at [email protected]

Europe Region: +44 778 256 0738

North America Region: +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Automotive | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Towards Dental | Towards EV Solutions | Nova One Advisor | Healthcare Webwire | Packaging Webwire | Automotive Webwire | Nutraceuticals Func Foods | Onco Quant | Sustainability Quant | Specialty Chemicals Analytics

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest

Disclaimer: The above press release comes to you under an arrangement with GlobeNewswire. NewIndiaObserver.com takes no editorial responsibility for the same.

Disclaimer: The above press release comes to you under an arrangement with GlobeNewswire. NewIndiaObserver.com takes no editorial responsibility for the same.