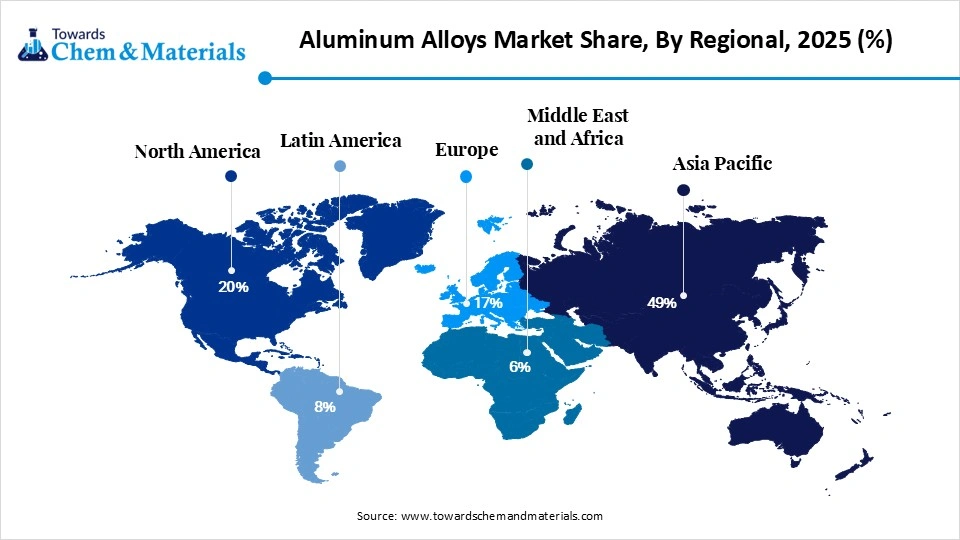

The global aluminum alloys market size reached USD 245.11 billion in 2025 and is expected to be worth around USD 475.45 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 6.85% over the forecast period from 2026 to 2035. Asia Pacific dominated the aluminum alloys market with the largest revenue share of 49% in 2025. A study published by Towards Chemical and Materials a sister firm of Precedence Research.

Ottawa, April 28, 2026 (GLOBE NEWSWIRE) — According to Towards Chemicals and Materials Analytics and Consulting, global aluminum alloys market was valued at USD 245.11 billion in 2025, is estimated to reach USD 261.90 billion in 2026, and is projected to reach USD 475.45 billion by 2035, growing at a CAGR of 6.85% from 2026 to 2035. In terms of volume, the aluminum alloys market is projected to grow from 82.55 million tons in 2025 to 147.14 million tons by 2035. growing at a CAGR of 5.95% from 2026 to 2035. Aluminum alloys market is growing due rising demand from automotive electrification, aerospace expansion, and supported by recycling initiatives and lightweight material adoption.

Don’t miss out on business opportunities in Aluminum Alloys Market. Speak to our analyst and gain crucial industry insights that will help your business grow. {Download a Sample Report Here@ https://www.towardschemandmaterials.com/download-sample/6356 }

What are the Factors Driving of the Aluminium Alloys Market?

The aluminium alloy field is developing quickly as various industries strive for environmentally friendly, lightweight, long-life materials. The International Energy Agency has reported more than 17 million electric cars were sold in 2024, greatly contributing to the demand for more efficient vehicles and greater battery ranges. Additionally, infrastructure expansion and renewable energy usage have increased the use of aluminium alloys throughout the world, such as in solar panels and as part of electric power transmission systems.

The International Aluminium Institute has also predicted additional increases due to greater amounts of scrap metal in recycling programs (aluminium retains 100% of its properties when recycled) and because between 70% and 95% of the total energy used in making one new aluminium plate from a scrap plate is less than what is required for creating it from bauxite/alumina. Government regulations promoting fuel economy and urban revitalization as well as through promotion of sustainable products will continue to increase long-term demand for aluminium alloys.

Aluminum Alloys Market Report Highlights

- By region, Asia Pacific dominated the market with a share of 49% in 2025 and is expected to be the fastest-growing region in the market, with a CAGR of 7.4% in the forecast period.

- By region, North America is notably growing with 20% market share in 2025.

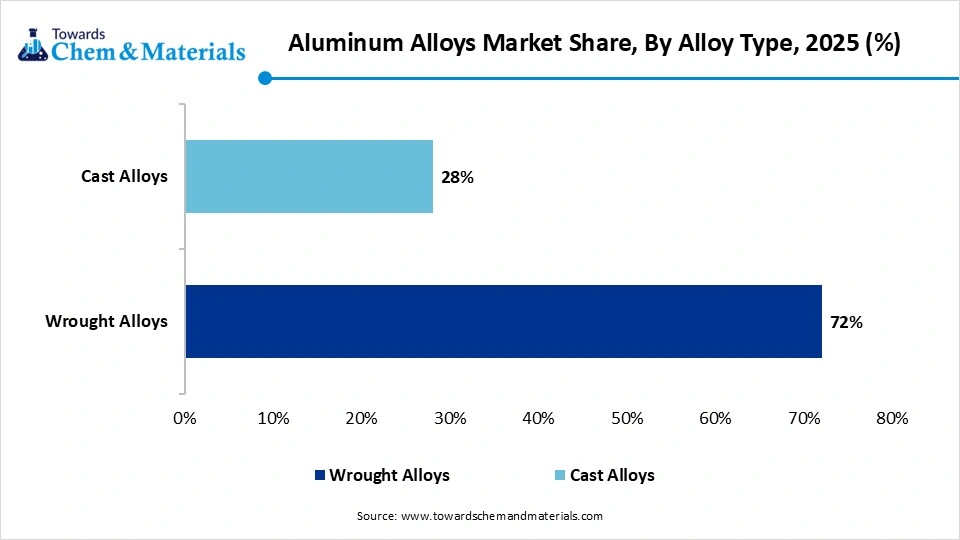

- By alloy type, the wrought alloys segment dominated the market with 72% share in 2025.

- By alloy type, the cast alloys segment held the 28% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.4% in the forecast period.

- By product form, the flat rolled products segment dominated the market with 46% share in 2025.

- By product form, the castings segment held the 17% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.5% in the forecast period.

- By processing method, rolling segment dominated the market with 41% share in 2025.

- By processing method, the casting segment held the 25% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.6% in the forecast period.

- By end-use industry, the automotive segment dominated the market with 34% share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.2% in the forecast period.

- By application, the structural components segment dominated the market with 29% share in 2025.

- By application, the body panels segment held the 18% market share in 2025 and is expected to be the fastest-growing in the market, with a CAGR of 7.3% in the forecast period.

At a glance

- Market Estimated Size (2026): USD 261.90 Billion | CAGR (2026–2035): 6.85%

- Market Projected Size (2035): USD 475.45 Billion

- Market Volume (2025): 82.55 Million Tons (MT) | Volume CAGR (2026–2035): 5.95%

- Market Projected Volume (2035): 147.14 Million Tons (MT)

- Market Pricing (2025):

- Average Manufacturing Price: USD 2,159/ton

- Average Selling Price: USD 2,658/ton

- Pricing CAGR (2025–2035): 3.9%

Request Research Report Built Around Your Goals: [email protected]

What Are the Different Types of Aluminum Alloy?

Aluminum alloys come in seven different categories, according to their chemical makeup, primary alloying elements, and physical characteristics. These are:

- 1000 Series (Pure)

- 2000 Series (Copper)

- 3000 Series (Manganese)

- 4000 Series (Silicon)

- 5000 Series (Magnesium)

- 6000 Series (Magnesium and Silicon)

- 7000 Series (Zinc)

1. 1000 Series (Pure Aluminum)

This series is made up of at least 99% aluminum, with only tiny amounts of other elements. Because of this, it offers excellent corrosion resistance, high thermal and electrical conductivity, and great flexibility (ductility). However, it’s relatively soft and not very strong.

Common uses: chemical storage tanks, electrical conductors, and rivets.

2. 2000 Series (Copper Alloys)

Copper is the main element added here, which significantly increases strength. These alloys can also handle high temperatures and are suitable for heat treatment. The trade-off is lower corrosion resistance compared to other series.

Common uses: aerospace components, military equipment, and high-performance parts.

3. 3000 Series (Manganese Alloys)

Manganese improves corrosion resistance and makes the material easier to shape. These alloys have moderate strength and are not heat-treatable, but they are easy to work with and weld.

Common uses: cookware, roofing sheets, automotive parts, and building materials.

4. 4000 Series (Silicon Alloys)

Silicon helps aluminum flow easily when melted, making this series ideal for casting. It also reduces shrinkage during cooling. These alloys have good wear resistance and moderate strength.

Common uses: engine components, automotive parts, and welding materials.

5. 5000 Series (Magnesium Alloys)

Magnesium increases strength while maintaining good corrosion resistance, especially in marine environments. These alloys are also strong and weldable.

Common uses: shipbuilding, pressure vessels, bridges, and sheet metal parts like aluminum 5052.

6. 6000 Series (Magnesium and Silicon Alloys)

This is one of the most versatile and widely used aluminum alloy groups. It offers a good balance of strength, corrosion resistance, and machinability. These alloys can also be heat-treated.

Common uses: structural components in construction, automotive parts, and aerospace applications. Aluminum 6061 is especially popular due to its affordability and versatility.

7. 7000 Series (Zinc Alloys)

Zinc is the main element in this high-strength series. These alloys are among the strongest aluminum materials available and can be heat-treated. They also offer good fatigue resistance but require careful handling during welding.

Common uses: aircraft structures, aerospace components, and high-performance sports equipment.

Aluminium Alloys Market Opportunity

The aluminium alloy market has strong growth opportunities powered by an energy transition and continued development of infrastructure. NITI Aayog estimates that India’s aluminium consumption will increase at a rate of approximately 4.4% p.a., due to significant urbanisation and forecasted growth rates of 4.4% for the overall economy and approximately 70% of anticipated infrastructure has still not been constructed as of 2047. The use of alloys is prevalent in electric vehicles, solar panel systems, and grid systems as their lightweight and corrosion-resistant characteristics are very important.

Recycling is a huge opportunity for the aluminium industry, with secondary aluminium projected to provide up to 50% of the world’s aluminium supply in the long term and thereby increase the industry’s environmental sustainability. The most recent developments in the aluminium industry include increasing demand for scrap metal due to a growing demand for recycled aluminium and policy discussions that will ease imports of primary aluminium into the country, which will provide a consistent supply of aluminium for downstream manufacturers of aluminium alloys and create new opportunities for a circular economy.

Immediate Delivery Available | Buy This Premium Research Report (Global Deep Dive

USD 3200) https://www.towardschemandmaterials.com/checkout/6356

Aluminum Alloys Market Report Scope

| Report Attribute | Details |

| Market Size and Volume in 2026 | USD 261.9 Billion / 87.46 Million Metric Tons |

| Expected Size and Volume by 2035 | USD 475.45 Billion / 147.14 Million Metric Tons |

| Growth rate | CAGR of 6.85% from 2026 to 2035 |

| Base year for estimation | 2025 |

| Historical data | 2021 – 2025 |

| Forecast period | 2026 – 2035 |

| Quantitative Units | Volume in Kilotons, Revenue in USD million/billion, and CAGR from 2026 to 2035 |

| Report coverage | Volume forecast, revenue forecast, competitive landscape, growth factors, and trends |

| Segments covered | By Alloy Type, By Product Form, By Processing Method, By End-Use Industry, By Application and By Region |

| Regional scope | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Country scope | U.S.; Canada; Mexico; Germany; UK; France; Spain; Italy; Russia; China; India; Japan; South Korea; Brazil; GCC; South Africa |

| Key companies profiled | Alcoa Corporation; AluminIum BahraIn B.S.C. (Alba); Aluminum Corporation of China; Hindalco; Hydro; National Aluminum Company Limited; Novelis; Press Metal; RusAL; UACJ Corporation |

For more information, visit the Towards Chemical and Materials website or email the team at [email protected]| +1 804 441 9344

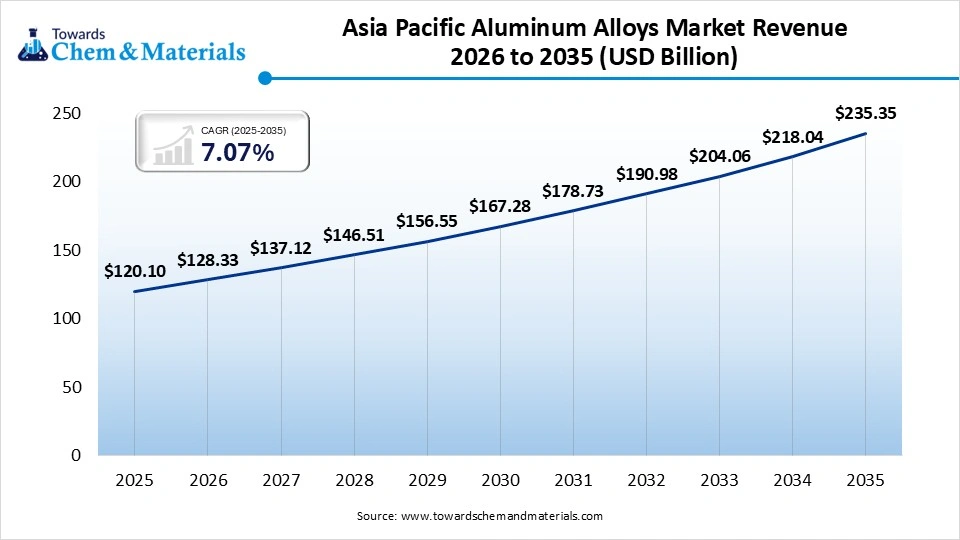

Why Is the Asia-Pacific Region the Dominant in Aluminium Alloys Market?

The Asia Pacific aluminum alloys market size was estimated at USD 120.10 billion in 2025 and is projected to reach USD 235.35 billion by 2035, growing at a CAGR of 7.07% from 2026 to 2035

Asia Pacific has emerged as a leading player in the aluminium alloy market is because of its established manufacturing base as well as the rapid growth of its economies and the demand from the automotive, construction, and electronics. Countries in the Asia-Pacific region, including China, India, and Japan, are producing/consuming large amounts of aluminium alloys. In the Asia-Pacific region, favourable manufacturing conditions exist, including low-cost labour and sufficient capacity to process raw materials, along with the continued growth of infrastructure projects, all support this sector’s ability to dominate aluminium alloys production throughout the world. An increase in the number of electric vehicles and new technologies to produce renewable energy have a positive impact on aluminium alloys usage and there are also many government programs that support local manufacturers and/or the exporting of products support the overall growth of the aluminium alloy market in the Asia-Pacific region.

What Is Driving the Rapid Growth of North America’s Aluminium Alloy Market?

Because of the increased demand for lightweight and high-strength materials as a result of technological advances in the aerospace, automotive, and defence industries in North America, the aluminium alloy market is growing rapidly in North America. Advanced manufacturers, such as Alcoa Corporation, are producing innovative new alloys. Additionally, with the increase in production of electric vehicles and a desire to improve fuel economy in traditional automobiles, there will be increased use of aluminium in these vehicles. Furthermore, with new investments into sustainable manufacturing and sustainable recycling technologies, there is potential for continued large-scale growth of the aluminium alloy market in North America. Government incentives and support of clean energy and domestic manufacturing will help create new opportunities for growth in the aluminium alloy market, and the ongoing introduction of new and improved alloys will continue to create numerous new applications for aluminium alloys in many industries.

Immediate Delivery Available | Buy This Premium Research Report@https://www.towardschemandmaterials.com/download-sample/6356

Aluminum Alloys Market Segmentation Insights

Alloy Type Insights

Why is Wrought Alloys the leading Segment in Aluminium Alloys Market?

Wrought Alloys continue to dominate the market due to their high mechanical strengths, superior corrosion resistance, and ability to be rolled or extruded into shapes useful in manufacturing processes and applications as well as being strong enough to withstand transportation and construction activities needing to be durable yet lightweight. Wrought alloys have the capability of being formed into sheets, plates, and profiles, thereby making them significantly useful for large volume manufacturing processes and applications.

Cast alloys have been slower to gain ground than wrought, they have proven to be attractive alternatives with many manufacturers for their lower-cost alternatives for producing complex-shaped product requiring intricate designs. As such, cast alloys are being used more and more in the automobile and machinery industries, where their use offers many advantages over wrought alloys. Additionally, new casting technologies and the growing demand for lightweight engine components as well as components for electric vehicles has significantly increased the use of castings across the entire manufacturing sector.

Product Form Insights

Which Product Form Dominates the Aluminium Alloys Market?

Flat Rolled Products or Sheets, Plates & Foils are dominating in regard to their high utilization in many different applications, such as Packaging, Automotive Panels & Construction Materials. Flat Rolled Products provide great Formability & Surface Finish, which gives you an excellent material option when requiring a Strong material that is also lightweight. The demands for Sustainable Packaging & Energy Efficient Vehicles continue to drive the growth of Flat Rolled Products.

Castings are also growing rapidly due to increasing demand for Precision Engineered Components in the Automotive & Industrial Industries. Castings allow for manufacturing of complex geometries while using minimal amount of Material. The continued growth of Electric Vehicles & Machinery Manufacturing will continue to create high demand for ‘high performance’ Cast Aluminium components.

Processing Method Insights

Why Packaging Segment Dominates the Aluminium Alloys Market in 2025?

Rolling is the primary processing method because it can produce large quantities of uniform aluminium sheets or plates at a high speed. Hot or cold rolling techniques can improve the quality of both the strength and surface of the sheet. Businesses in industries such as packaging, automotive, and construction rely on rolled products for consistency and efficiency in large-scale manufacturing.

Casting is expected to grow at the fastest CAGR over the forecast period. due to its ability to create complex and custom-designed components. High-precision die casting and investment casting techniques are being adopted to minimise the amount of machining required post-production. There is an increasing demand from manufacturers of automobiles and industrial equipment for more lightweight products resulting in a significant adoption of advanced casting technologies.

End-Use Industry Insights

Which End User Segment Dominating in 2025?

By end-use industry, the automotive segment dominated the market in 2025 and is expected to be the fastest-growing in the market, as a result of an increase in the demand for lightweight materials, such as aluminium, to increase fuel efficiency and decrease pollution. The usage of aluminium alloy materials in passenger car manufacturing, commercial vehicle manufacturing, and especially in electric vehicle manufacturing, is prevalent. Additionally, the automotive industry is adopting new designs for vehicles, and the push for increased regulation of sustainability has led to further adoption of aluminium by this industry. Moreover, as electric vehicles become more popular, and as new formulations of aluminium alloys continue to emerge, the automotive industry will be able to maintain its position as both the largest and fastest-growing industry segment.

Application Insights

Why Structural Components Are the Leading Application Segment?

Structural components dominate because they provide the foundation, the strength, and stability necessary for all types of construction (buildings, automobiles, and aerospace). Due to their excellent strength-to-weight ratios, aluminium alloys are very effective in supporting load-bearing structures. Their corrosion resistance and high durability extend their potential use as long-term structural materials.

The body panels segment is expected to be the fastest-growing in the market, with a CAGR in the forecast period, driven by the high demand for lightweight vehicles and fuel-efficient vehicles. Aluminium alloys allow the weight of the vehicle to be reduced while still maintaining the safety and design flexibility of the vehicle. The increasing use of electric vehicles and the ongoing changes in the styling of new automobiles are having a large impact on the consumption of aluminium in exterior car parts.

More Insights in Towards Chemical and Materials:

- High Strength Aluminum Alloys Market Size to Hit USD 204.07 Bn by 2035

- Carbon Coated Aluminum Foil Market Size to Hit USD 8.5 Bn by 2035

- Coating Materials Market Size to Surpass USD 345.63 Billion by 2035

- Aluminum Flat Products Market Size to Hit USD 112.15 Bn by 2035

- Aluminum Metal Powder Market Size to Hit USD 4.15 Billion by 2035

- Aluminum Extrusion Market Size to Surpass USD 224.18 Bn by 2035

- Aluminum Casting Market Size to Surpass USD 172.05 Bn by 2035

- Ferro Alloys Market Size to Surpass USD 132.88 Billion by 2035

- Toluene Diisocyanate Market Size to Hit USD 13.35 Billion by 2035

- Aluminum Composite Materials Market Size to Reach USD 8.18 Billion by 2034

- Aluminum Foil Market Size to Reach USD 48.46 Billion by 2034

- Aluminum Trihydrate (ATH) Market Volume to Hit 4653.45 Kilo Tons by 2034

- Aluminum Oxide Market Volume to Hit 215.45 Million Tons by 2034

- Shape Memory Alloys Market Size to Hit USD 46.44 Bn by 2034

- C5 Fraction Market Size to Hit USD 6.67 Billion by 2035

- Steel Decarbonization Market Size to Surpass USD 434.33 Bn by 2035

- Specialty Gas Market Size to Hit USD 27.12 Bn by 2035

- Specialty Fats & Oils Market Size to Surpass USD 34.13 Bn by 2035

- Industrial Fasteners Market Size to Hit USD 174.01 Bn by 2035

- Aluminum Alloys Market Size to Hit USD 475.45 Billion by 2035

- Boron Nitride Powder Market Size to Hit USD 3.3 Billion by 2035

- Olefin Polymerization Catalyst Market Size to Surpass USD 9.15 Bn by 2035

- Hexylene Glycol (HG) Market Size to Surpass USD 3.21 Billion by 2035

- Aqua Ammonia Market Size to Hit USD 4.85 Billion by 2035

- Isopropyl Alcohol Market Size to Hit USD 8.39 Billion by 2035

- Ethylene Alpha Olefin Copolymers Market Size to Surpass USD 133.36 Bn by 2035

- 1,3 Butadiene Market Size to Hit USD 4.95 Billion by 2035

- Plastic To Fuel Market Size to Surpass USD 14.83 Billion by 2035

- Liquefied Waste Plastic Market Size to Hit USD 10.3 Bn by 2035

Aluminum Alloys Market Top Key Companies:

- Alcoa Corporation

- AluminIum BahraIn B.S.C. (Alba)

- Aluminum Corporation of China

- Hindalco

- Norsk Hydro

- National Aluminum Company Limited

- Novelis

- Press Metal

- RusAL

- UACJ Corporation

Aluminum Alloys Market Recent Developments

- In February 2026, National Aluminium Company Limited (NALCO) launched its IA91 grade aluminium alloy ingot, a silicon-based high-performance material designed for advanced casting applications, enhancing strength, corrosion resistance, and expanding its value-added product portfolio.

- In October 2025, EGA Spectro Alloys announced phase-two expansion of its Minnesota recycling facility, adding nearly 100 million pounds annual billet capacity, aiming to significantly boost aluminium recycling output and support sustainable production growth by 2027.

- In June 2024, Bharat Forge announced investment of USD 40 million for its subsidiary BFA in U.S., which focused on aluminum components for automotive industry. With this investment, the company plans to increase its capital expenditure and improve its footprint in the U.S.

Aluminum Alloys Market Report Segmentation

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2019 to 2035. For this study, Towards Chemical and Materials has segmented the global Aluminum Alloys Market

By Alloy Type

- Wrought Alloys

- 1xxx Series (Pure Aluminum)

- 2xxx Series (Al-Cu)

- 3xxx Series (Al-Mn)

- 5xxx Series (Al-Mg)

- 6xxx Series (Al-Mg-Si)

- 7xxx Series (Al-Zn)

- Cast Alloys

- Al-Si Alloys

- Al-Cu Alloys

- Al-Mg Alloys

- Others

By Product Form

- Flat Rolled Products

- Sheets

- Plates

- Foils

- Extruded Products

- Rods & Bars

- Profiles

- Castings

- Forgings

By Processing Method

- Rolling

- Hot Rolling

- Cold Rolling

- Extrusion

- Casting

- Die Casting

- Sand Casting

- Investment Casting

- Forging

By End-Use Industry

- Automotive

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles

- Aerospace & Defense

- Construction

- Residential

- Commercial

- Packaging

- Beverage Cans

- Food Containers

- Electrical & Electronics

- Marine

- Industrial Machinery

By Application

- Structural Components

- Body Panels

- Conductors

- Packaging Materials

- Heat Exchangers

- Others

By Regional

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Immediate Delivery Available | Buy This Premium Research Report@

https://www.towardschemandmaterials.com/checkout/6356

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

To find out more, visit www. Towards Chemicals and Materials Analytics and Consulting ™.com or follow us on Twitter, LinkedIn

Contact:

Towards Chemicals and Materials Analytics and Consulting

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Visit Our Website: https://www.towardschemandmaterials.com/

Disclaimer: The above press release comes to you under an arrangement with GlobeNewswire. NewIndiaObserver.com takes no editorial responsibility for the same.

Disclaimer: The above press release comes to you under an arrangement with GlobeNewswire. NewIndiaObserver.com takes no editorial responsibility for the same.